Is the IPO Landscape Improving?

After nearly three years of subdued activity, the global IPO market is stirring again. The change hasn’t come in a single wave but rather as a series of steady ripples—each quarter slightly stronger than the one before. The first half of 2025 saw a modest rebound in listings and proceeds, and by late summer, the long-closed IPO window for venture-backed companies slowly began to crack open.

For investors, this is more than a sign of market health—it starts to restore a vital source of liquidity. IPOs remain a key exit route in venture capital, and their gradual reopening offers long-awaited visibility on future distributions.

Early green shoots

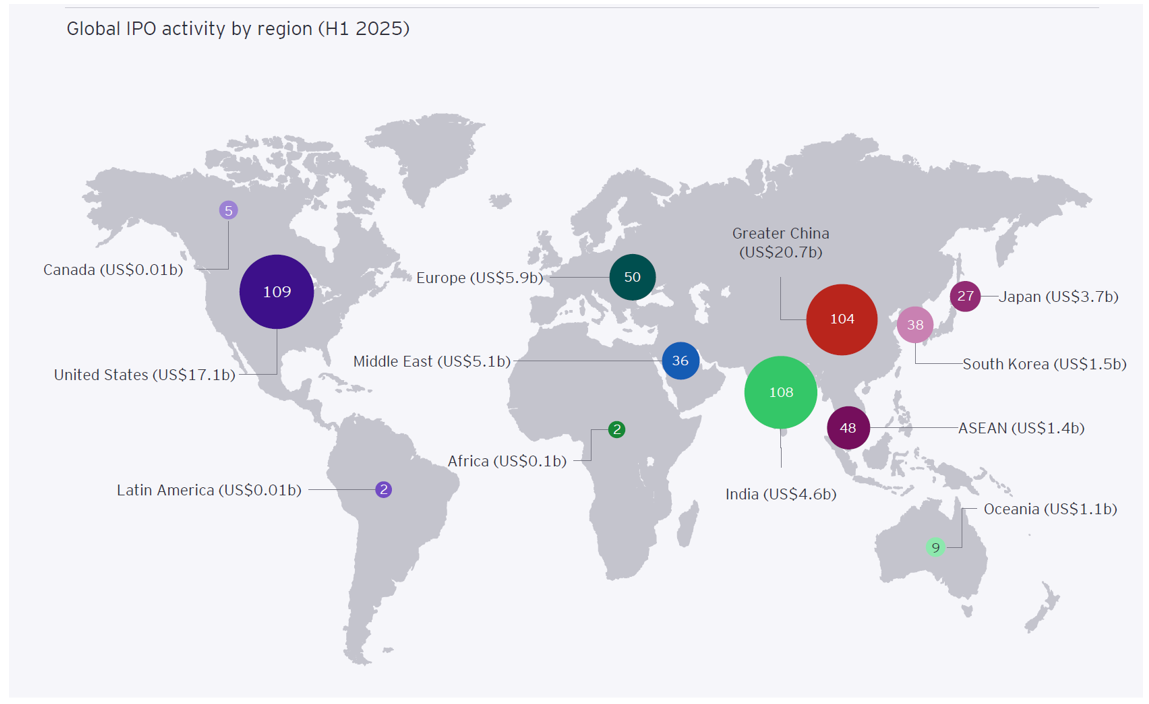

The story of the recovery is gradual but visible. In the first half of 2025, global IPO proceeds climbed back above the sixty-billion-dollar mark, roughly a 17 percent improvement over the same period of last year. For the first time since 2021, several regions moved in the same direction: the United States, although starting from a low base, recorded its busiest month of new listings in nearly four years, India and the Middle East held steady, and Greater China re-emerged as a key driver of issuance.

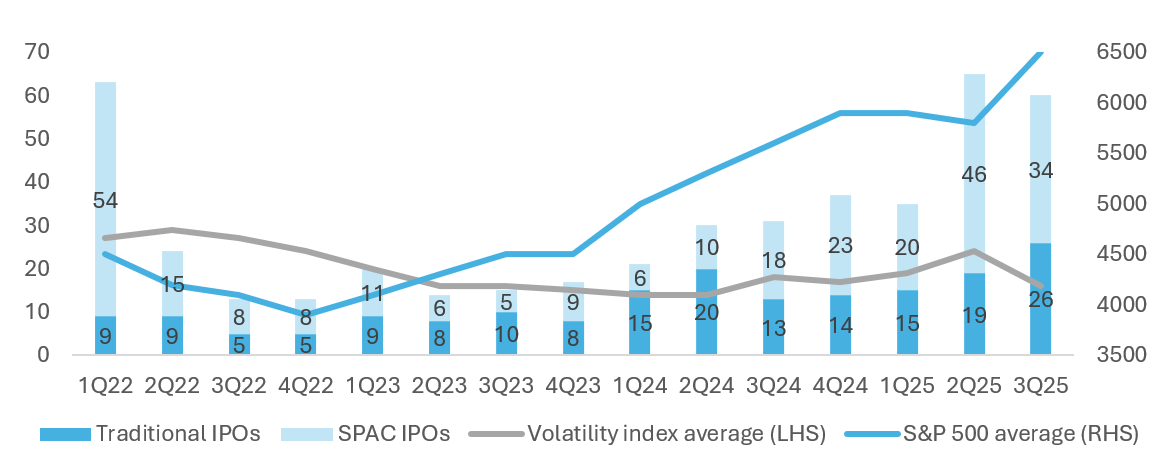

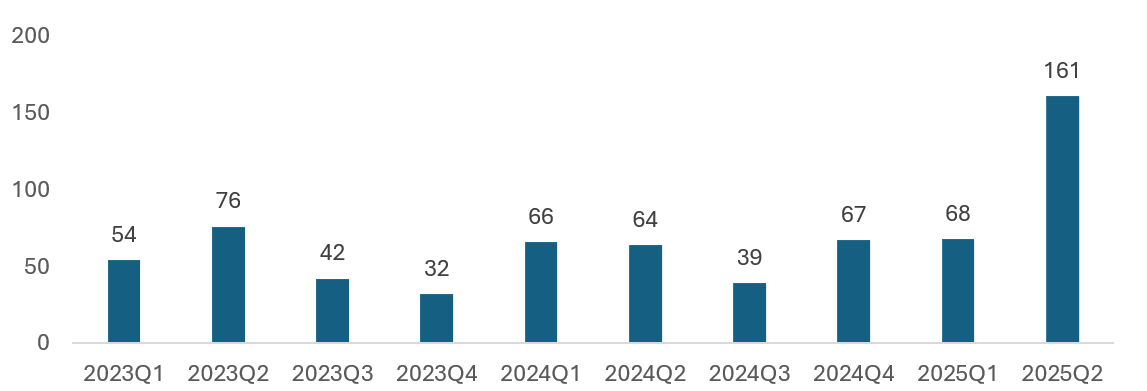

What stands out most is the renewed participation of late-stage venture names. After multiple quarters of hesitation, a few well-known tech companies tested public markets—and found buyers waiting. By the end of the third quarter, more than sixty IPOs in the U.S. alone had raised nearly thirty billion dollars, up roughly a third from the same period last year. September was particularly strong, with thirteen listings worth more than eight billion dollars. Pricing discipline returned too: more than half of those offerings priced at or above their target range, and average first-day gains exceeded thirty percent.

Number of U.S. IPOs vs S&P 500 and VIX by Quarter

Behind the numbers lies a more balanced tone. Investors are again cautiously willing to reward growth, but only when it comes with profitability and operational maturity. Deals that met those criteria performed well—such as Figma’s or CoreWeave’s successful listings—while others that lacked profitability or clear growth visibility, including several U.S. consumer-tech IPOs—such as Klarna or Stubhub—, struggled to maintain traction post-listing. The new standard seems clear: companies entering public markets must demonstrate scale, sustainable margins, and readiness to operate as public entities from day one.

A market that rewards discipline

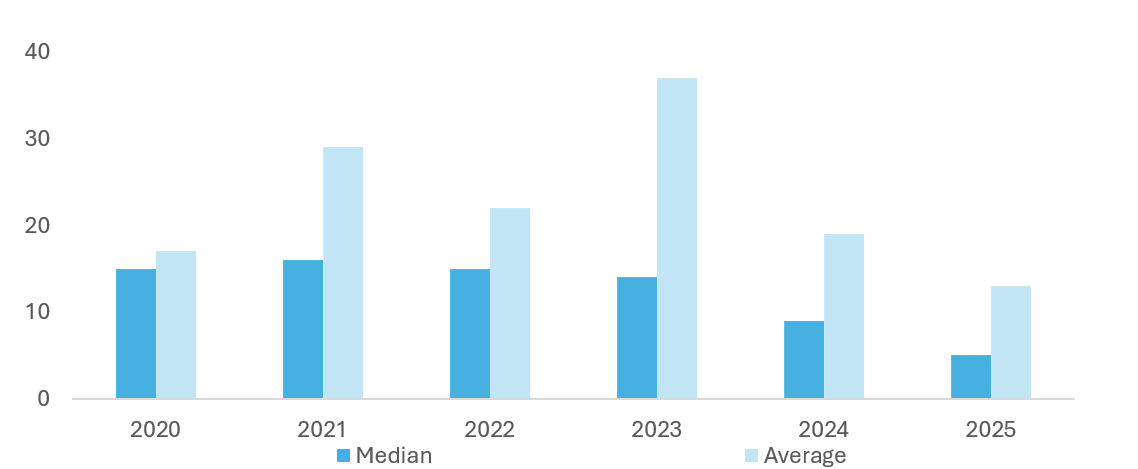

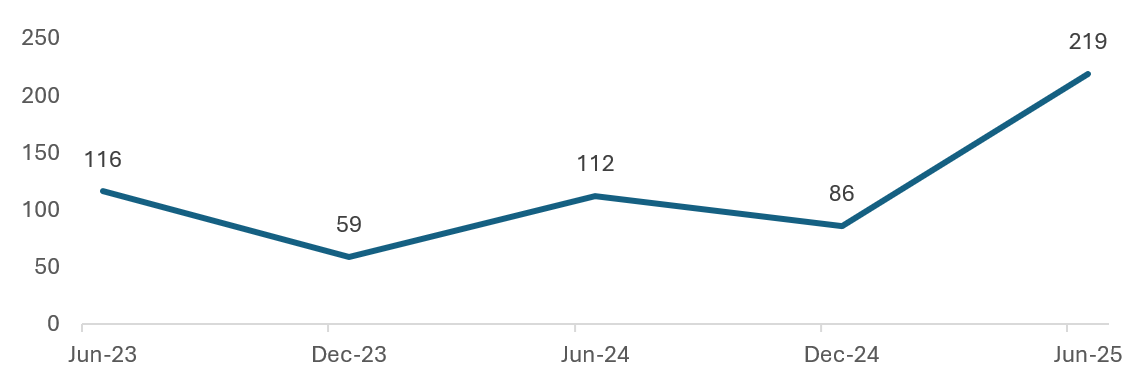

The shift in sentiment is not about exuberance—it’s about standards. After the overheated cycle of 2021, valuation expectations have reset to more sustainable levels. Median revenue multiples for new listings hover near four times sales, a fraction of the peak years when some companies commanded more than four times that figure. Roughly one in four issuers this year are already profitable, compared with virtually none during the last major wave of venture-backed IPOs.

Valuation-to-Revenue Multiple for startup IPOs

This renewed focus on fundamentals has re-defined what it means to be “IPO-ready.” The path to market now rewards companies with strong cash generation, visible growth engines, and governance structures built for scrutiny. The lesson for founders and investors alike is that public investors will pay for quality—but not for promises.

Beyond the U.S.: Hong Kong’s dramatic comeback

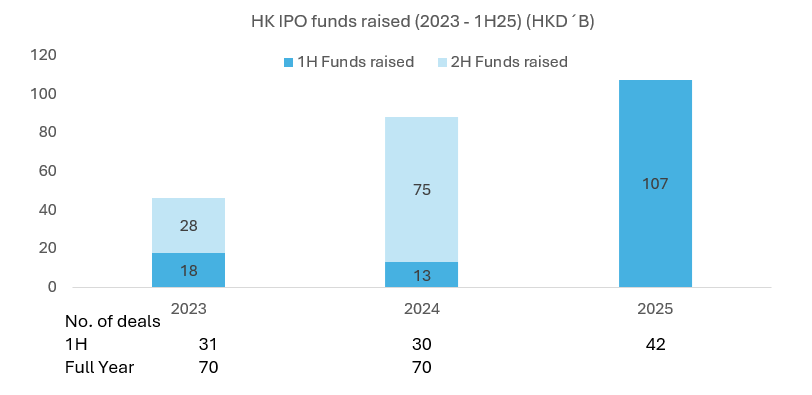

The revival is not confined to Wall Street. In Asia, Hong Kong has staged a significant improvement this year and, once again, its technology leading the charge. The first half of 2025 brought more than forty new listings that collectively raised over thirteen billion U.S. dollars—about seven times the amount raised in the same period a year earlier. The surge was powered by large technology and new-economy companies from mainland China choosing Hong Kong as their listing venue, often through dual A + H structures that link domestic and international capital.

HK IPO Funds Raised (2023 – 1H 2025) (HKD’B)

The exchange’s specialist channels for tech and biotech firms—expanded this year under its “TECH” framework—have shortened processing times and increased flexibility for earlier-stage innovators. As a result, the city’s pipeline of potential listings is at record highs, with more than two hundred applications awaiting review. For high-growth tech issuers, Hong Kong has re-emerged as both a regional and global exit hub, offering access to deep liquidity and investors eager for exposure to Asian innovation.

HK IPO Active Pipeline (2023-1H 2025 YTD)

HK IPO Application Submition (2023-1H 2025 YTD)

Cautious optimism ahead

The data still call for restraint. Deal volumes remain well below long-term averages, and the window can narrow as quickly as it opens. Yet the character of the market is progressively changing in encouraging ways: fundamentals matter again, valuations are rational, and public investors are signalling renewed appetite for credible, profitable growth stories.

After several quiet years, the IPO landscape is improving—not explosively, but steadily. The reopening is in its early stages, fragile but genuine. If macro stability holds and recent listings continue to trade well, 2026 could mark the transition from a tentative revival to a sustained new cycle of public-market access for venture-backed technology companies.

2. IPOs in Galdana’s Portfolio(1)

The improvement in market sentiment has already begun to show up tangibly in Galdana’s own portfolio. After several quiet years with few realizations, a notable shift has taken place since the second quarter of 2025. Fourteen portfolio companies have successfully completed IPOs during this period, marking the most active listing environment we have seen in recent vintages. While these listings represent a major milestone, liquidity from them will probably begin to be realized gradually after the customary six-month lock-up periods, hopefully over the following quarters and/or years.

Collectively, these companies represented a pre-IPO net asset value of €60.6 million for Galdana’s Portolio(1). While that figure is modest relative to our total paid-in capital of €685 million across Galdana’s mature funds(2), it is a significant step in the right direction. It reflects the early stages of renewed liquidity across venture portfolios and confirms that exit channels are starting to reopen for high-quality assets.

Importantly, the performance of these newly listed companies invested by Galdana(1) has been particularly encouraging. On average, they now trade 51% (3) above their pre-IPO net asset value, a solid outcome that reflects both prudent valuation practices and healthy public-market demand. This uplift stems from two reinforcing dynamics: first, the IPOs were priced at 34% (4) premium to the last quarter’s NAV, confirming that private valuations had remained conservative; and second, the shares have continued to appreciate post-listing, rising a further 11% (5) on average in the aftermarket. Together, these movements highlight how disciplined valuation during the private phase, combined with renewed investor confidence in public markets, can translate into meaningful value creation for long-term investors.

Out of these 14 IPOs only 2 of them trade below the NAV valuation they had in the quarter prior to the IPO, what we see as the result of a healthy conservative valuation policy of the GPs invested by Galdana(1).

Perhaps most promising, these fourteen IPOs may represent only the first wave of what could be a broader liquidity cycle. Our pipeline of potential listings for the next twelve months remains potentially robust (c.€150m of NAV in Galdana’s mature funds(2)), encompassing a diverse set of companies across technology, healthcare, and fintech. Should market conditions stay supportive, we expect an acceleration in portfolio realizations—turning cautious optimism into measurable returns for our investors.

Footnotes:

- Source: Galdana Internal Data. As of 31-Oct-2025. Includes Galdana Ventures I FCR, Galdana Ventures II FCR, Galdana Ventures II SICAV-RAIF, Galdana Ventures III FCR, Galdana Ventures III SICAV-RAIF, Galdana Ventures Asia SICAV-RAIF, Galdana Ventures SPV I SICAV-RAIF, Galdana Ventures SPV II SICAV-RAIF, Galdana Ventures 2024 FCR and Galdana Ventures 2025 FCR. Past returns do not guarantee future returns

- Source: Galdana Internal Data.Includes Galdana Ventures I FCR, Galdana Ventures II FCR, Galdana Ventures II SICAV-RAIF

- Source: Galdana Internal Data.Weighted (based on pre-IPO NAV for Galdana) average. 67% if equally weighted average. IPOs representing on aggregate less than 2% of total pre-IPO NAV not considered.

- Source: Galdana Internal Data.Weighted (based on pre-IPO NAV for Galdana) average. 47% if equally weighted average. IPOs representing on aggregate less than 2% of total pre-IPO NAV not considered.

- Source: Galdana Internal Data.Weighted (based on pre-IPO NAV for Galdana) average. 16% if equally weighted average. IPOs representing on aggregate less than 2% of total pre-IPO NAV not considered.

IMPORTANT NOTICE:

This document has been prepared by Altamar CAM Partners S.L. (together with its affiliates “AltamarCAM“) for information and illustrative purposes only, as a general market commentary and it is intended for the exclusive use by its recipient. If you have not received this document from AltamarCAM you should not read, use, copy or disclose it.

The information contained herein reflects, as of the date hereof, the views of AltamarCAM, which may change at any time without notice and with no obligation to update or to ensure that any updates are brought to your attention.

This document is based on sources believed to be reliable and has been prepared with utmost care to avoid it being unclear, ambiguous or misleading. However, no representation or warranty is made as of its truthfulness, accuracy or completeness and you should not rely on it as if it were. AltamarCAM does not accept any responsibility for the information contained in this document.

This document may contain projections, expectations, estimates, opinions or subjective judgments that must be interpreted as such and never as a representation or warranty of results, returns or profits, present or future. To the extent that this document contains statements about future performance such statements are forward looking and subject to a number of risks and uncertainties.

This document is a general market commentary only, and should not be construed as any form of regulated advice, investment offer, solicitation or recommendation. Alternative investments can be highly illiquid, are speculative and may not be suitable for all investors. Investing in alternative investments is only intended for experienced and sophisticated investors who are willing to bear the high economic risks associated with such an investment. Prospective investors of any alternative investment should refer to the specific fund prospectus and regulations which will describe the specific risks and considerations associated with a specific alternative investment. Investors should carefully review and consider potential risks before investing. No person or entity who receives this document should take an investment decision without receiving previous legal, tax and financial advice on a particularized basis.

Neither AltamarCAM nor its group companies, or their respective shareholders, directors, managers, employees or advisors, assume any responsibility for the integrity and accuracy of the information contained herein, nor for the decisions that the addressees of this document may adopt based on this document or the information contained herein.

This document is strictly confidential and must not be reproduced, or in any other way disclosed, in whole or in part, without the prior written consent of AltamarCAM.