Private Debt Market Review: Separating Media Noise from Structural Fundamentals

Recent weeks have seen a renewed wave of scrutiny on private debt markets, driven by a combination of idiosyncratic credit events, liquidity dynamics in semi-liquid vehicles, and broader macroeconomic uncertainty. Headlines have increasingly questioned the resilience of the asset class in a context defined by persistent inflation, elevated interest rates, and rising geopolitical tensions.

However, a rigorous and technically grounded analysis suggests a more nuanced conclusion: while the cycle is clearly maturing and dispersion is increasing, the structural foundations of private debt remain intact. The current environment calls neither for complacency nor alarmism, but for disciplined optimism anchored in selectivity and risk management.

The purpose of this report is to separate short-term noise from the structural fundamentals of the asset class, offering a balanced view: reassuring in terms of systemic solvency, yet prudent regarding the risks that characterize the current phase of the market.

Recent headlines have focused on three main areas:

- Idiosyncratic situations such as First Brands and Tricolor.

- The activation of redemption limits in certain semi-liquid vehicles.

- Risk narratives linked to artificial intelligence disruption, particularly in software.

A technical analysis of each of these elements helps distinguish temporary noise from the industry’s structural foundations.

1. Idiosyncratic Situations: First Brands and Tricolor

First Brands and Tricolor have been presented as examples of structural vulnerability in private debt. However, a detailed analysis suggests that these are highly specific situations and not representative of core senior secured sponsor-backed direct lending.

First Brands was linked to complex structures with collateral over receivables, documentation controversies, and double pledging of assets. The identified risks are characteristic of asset-based financing with high operational complexity, not traditional corporate lending with robust financial covenants.

Tricolor featured a unique credit profile associated with subprime financing, granular collateral, and a dynamic different from middle-market sponsor-backed companies with stable EBITDA generation.

In both cases, the determining factors were specific to the business model and the particular structuring involved. Moreover, both cases included alleged irregularities that became subject to legal proceedings. They therefore do not appear to constitute evidence of generalized deterioration in underwriting standards in the core segment, but rather cases with highly specific structural and governance characteristics. Extrapolating these events to the entire asset class oversimplifies the technical reality.

2. Redemption Limits in Evergreen and Semi-Liquid Vehicles

- These limits (typically 5% of quarterly NAV, subject to proration) are explicitly part of the product design as protection mechanisms against liquidity mismatches.

- They do not constitute extraordinary discretionary “gates,” but structural mechanisms to avoid forced sales of inherently illiquid assets at discounts in order to protect all investors.

Their activation reflects a temporary increase in liquidity demand, not necessarily underlying credit deterioration. Nevertheless, they do highlight two important structural considerations:

- Mismatch between perceived and actual liquidity, particularly among retail-oriented products.

- Behavioral sensitivity of investor bases in volatile macro environments.

Therefore, while not an automatic sign of a solvency crisis, they underscore the importance of properly aligning investor time horizons with the illiquid nature of the asset, as well as the need for responsible product distribution.

3. Artificial Intelligence and Software Exposure

- EBITDA sensitivity to technological disruption,

- Leverage levels, and

- Structural protection margins (equity cushion, covenants, and seniority).

Senior debt maintains priority of payment, negotiating capacity, and, in many cases, financial covenants that allow for early intervention. AI increases dispersion between winners and losers but does not invalidate the structural protection logic of senior tranches. That said, in scenarios of accelerated disruption, EBITDA erosion may occur more quickly than in traditional cycles, reducing reaction time even in senior structures. For this reason, sector analysis and the identification of companies with high operational criticality will be key in the coming years.

Market Indicators and Aggregate Data

Once the factors fueling media noise are contextualized, aggregate indicators of the private debt market show relative stability.

Yields have declined across all income-oriented assets, including private debt. However, according to the Cliffwater Direct Lending Index (CDLI), a widely used benchmark for U.S. direct lending, returns in 2025 were 9.33%, including expected unrealized losses from price markdowns of 54 bps. Spreads and SOFR have stabilized, leading Cliffwater to believe that current yields are sustainable.

Return generation continues to be supported by contractual carry, predominantly floating rate, which has captured elevated base rates during the recent cycle.

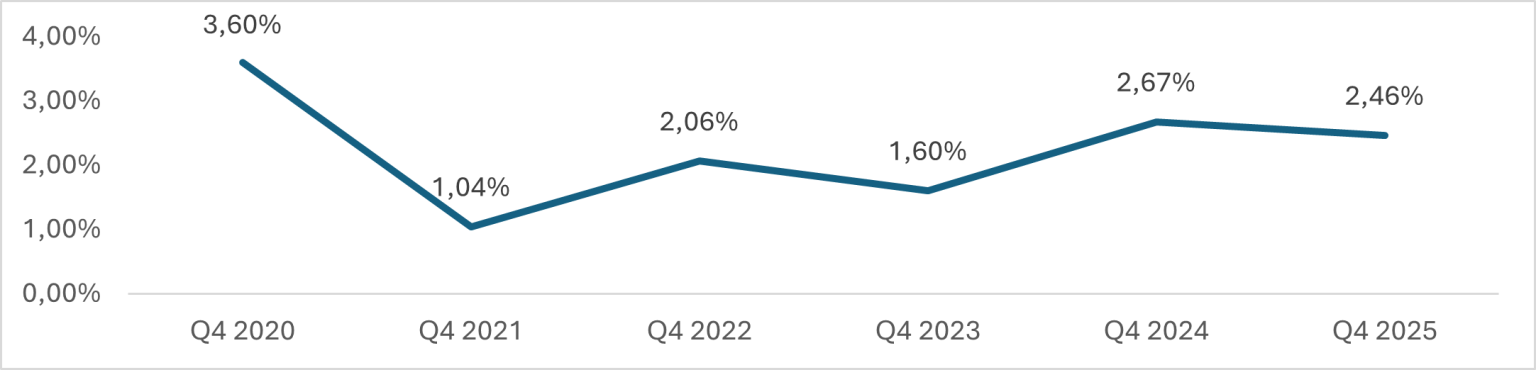

In addition, default rates are consistent with a mature phase of the cycle but remain far below from systemic crisis scenarios such as 2008–2009 or even the 2020 shock.

Proskauer Private Credit Default Index

Source: Proskauer’s Private Credit Default Index” As of January 26th, 2026

A good indicator that would contribute to prove credit quality and stability is that GP-led secondary transactions involving continuation vehicles are being executed at par or near par.

Illiquidity Premium and Market Segmentation

The illiquidity premium remains a key structural component. Although some spread compression1 has been observed in the upper mid-market (around 50–100 bps for higher-quality profiles), the lower mid-market continues to offer spreads 100–200 bps higher, in addition to OID and additional fees.

1. Source: Analysis by the AltamarCAM Private Credit team based on the overall market situation

This structural difference versus more competitive segments reflects reduced access to syndicated financing and greater operational intensity, maintaining attractive compensation for illiquidity. Structural seniority, the presence of real collateral, and direct negotiation capacity with sponsors also provide stronger downside protection mechanisms than liquid syndicated markets.

Manager Dispersion and AltamarCAM Positioning

- Approximately 3,000 loans in the portfolio, providing broad and representative middle-market diversification.

- Gross return at the loan level of around 10%, in line with top market references (Cliffwater Direct Lending Index).

- Illiquidity premium versus broadly syndicated loans (BSL) exceeding 250 bps (253 bps in the U.S. and 265 bps in Europe).

- Realized losses since inception 10 years ago totaling only 7 basis points, substantially below estimated aggregate market default levels.

- Software exposure of 14%, significantly below certain broad BDC universes, reducing sector concentration risk.

- Average loan-to-value of 38%, implying a robust equity cushion and a senior position in the capital structure that protects against moderate deterioration in enterprise value and provides important structural protection in pressured sectors such as Software/SaaS.

2. Source: AltamarCAM. Includes the following private debt funds: Altamar Private Debt I, Altamar Private Debt III, Altamar Private Debt IV, and AltaCAM Global Credit II. Note: Past returns are not necessarily indicative of future results given that the current economic conditions are not comparable to prior conditions, which may not repeat in the future. There are no guarantees that the funds will have similar results as previous funds.

Current Risks

Despite structural elements that insulate fundamentals from media noise, a realistic approach requires acknowledging current market risks:

- 2026–2027 Refinancings: Structures originated in 2021–2022 with aggressive multiples and adjusted EBITDA assumptions will face maturities in a less accommodating environment. Pressure may emerge in refinancings and selective restructurings.

- Spread Compression in Competitive Segments: Competition in the upper mid-market has reduced spreads and, in some cases, strained origination discipline.

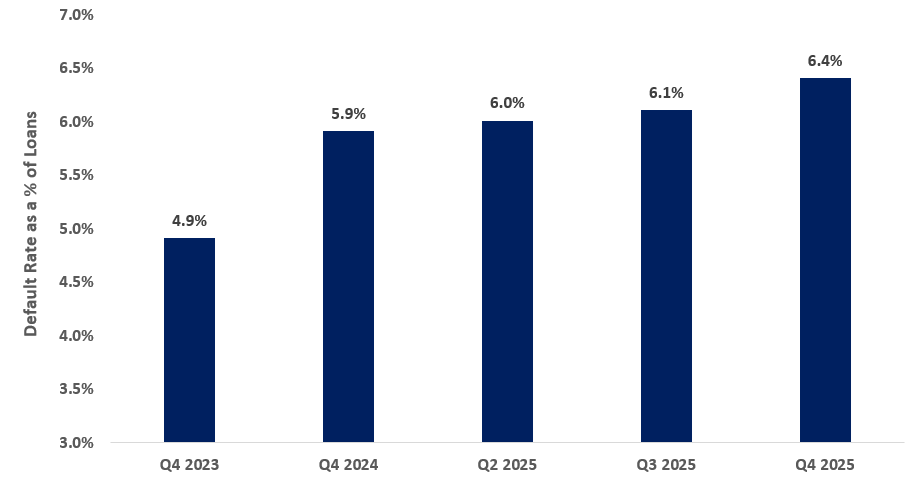

- Increase in Early Stress Metrics: Rising non-accruals, growing use of PIK, and amend-and-extend dynamics may signal tensions in certain portfolios. The “shadow default rate” in Lincoln’s index implies bad PIK rate rose from about 4.9% in Q4 2023 to 5.9% in Q4 2024, then to about 6.4% in Q4 2025

Private Credit ‘Bad PIK’ / Shadow Default Rate

Source: Lincoln International, Private Market Perspectives: U.S. Edition

- Sector Concentration: Elevated exposure to software in certain universes may amplify sensitivity to technological disruption.

We are not facing a systemic crisis, but rather an environment where dispersion will increase and asset class beta will be less decisive than selection alpha.

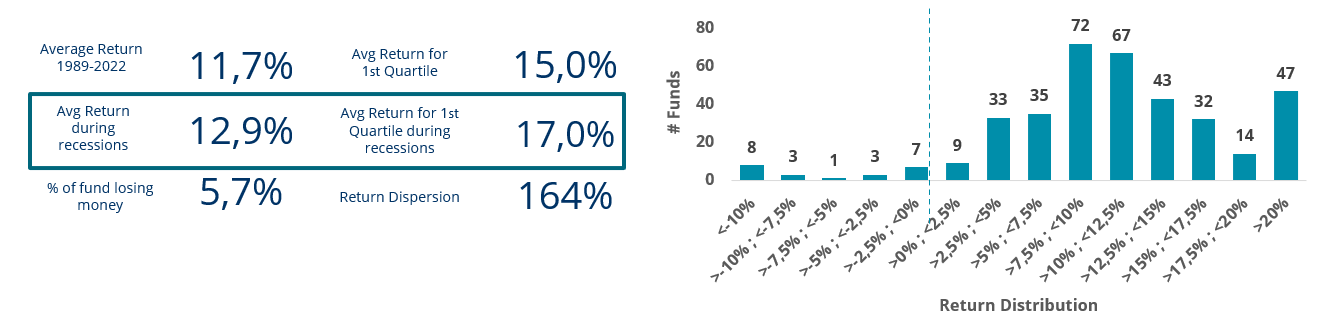

Distressed and Opportunistic Opportunities

This environment creates fertile ground for distressed and opportunistic strategies. The combination of widening spreads in special situations, the need for fresh capital in stressed structures, and the potential for secondary transactions in portfolios at discounts opens opportunities for managers with legal-operational analytical capabilities and mandate flexibility.

Opportunistic Credit Return Distribution

Source: Preqin and AltamarCAM Credit. Analysis done by Altamar using Preqin database. Total sample size of 388 funds. Sample size includes funds with a focus on North American and/or Europe with a size >$200Mn. Past returns are not necessarily indicative of future results given that the current economic conditions are not comparable to prior conditions, which may not repeat in the future. There are no guarantees that the funds will have similar results as previous funds.

Historically, distressed funds launched during phases of credit normalization have captured attractive returns through discounted acquisitions and active participation in restructuring processes.

Conclusion

- High contractual returns,

- Diversification versus public markets, and

- Structural protection mechanisms in moderate downturn scenarios.

Nevertheless, investors must pay close attention to:

- Vehicle liquidity,

- Sector concentration (including but not limited to software),

- Origination discipline in a tighter spread environment, and

- The evolution of early stress indicators such as non-accruals, PIK, and amend-and-extend activity.

We are facing a market evolving toward greater differentiation. In this phase, capital preservation and return generation will depend less on broad access to the asset class and more on the structural quality of investments and active risk management capability.

IMPORTANT NOTICE:

This document contains information subject to change regarding Altamar CAM Partners, S.L., Altamar Private Equity, SGIIC SAU, CAM Alternatives GmbH and their subsidiary and affiliated companies (collectively referred to as “AltamarCAM”), as well as other funds and vehicles actively managed or advised by AltamarCAM (the “Funds”). It has been prepared for informational and illustrative purposes, as a general market commentary, and is provided for the exclusive use of its intended recipient. If you did not receive this document directly from AltamarCAM, you should not read, use, copy, or share it.

The information contained in this document reflects, as of the date of publication, AltamarCAM’s views, which may change at any time without prior notice. AltamarCAM is under no obligation to update it or to provide any potential updates.

This document is based on sources considered reliable and has been prepared with the utmost care to avoid being unclear, ambiguous, or misleading. However, no representation or warranty is made regarding its truthfulness, accuracy, or completeness, and it should not be regarded as such. AltamarCAM assumes no responsibility for the information contained in this document.

This document may contain projections, expectations, estimates, opinions, or subjective judgments, all of which must be interpreted as such and never as a statement or guarantee of present or future results, performance, or returns. To the extent that this document contains statements about future performance, such statements are forward‑looking and subject to a number of risks and uncertainties. Past performance is not necessarily indicative of future results, as current economic conditions are not comparable to those that existed previously and may not repeat in the future. There is no guarantee that the Funds will achieve results comparable to previous funds. Nor are there guarantees regarding specific returns, asset diversification, the materialization of assumptions (regarding the market, its stability, its risks, or any other matter), or the fulfillment of any particular strategy, approach, or investment objective. All of the foregoing will depend, among other factors, on the operating performance of the Funds’ portfolio companies, asset values and market conditions at the time of sale, transaction-related costs, and the timing and method of exit—all of which may differ from the assumptions used in the data contained herein. Consequently, returns are not guaranteed: product values are subject to market fluctuations, these forecasts do not represent a reliable indicator of future results, and such returns may be zero or even negative. Investors should bear in mind that any returns generated are subject to taxation, which will depend on each investor’s individual circumstances and may change in the future.

This document is solely a general market commentary and should not be interpreted as regulated advice, an investment offer, a solicitation, or a recommendation. Alternative investments may be highly illiquid, speculative, and may not be suitable for all investors. Investment in alternative assets is intended only for experienced and sophisticated investors who are willing to assume the significant economic risks associated with such investments. Prospective investors in any alternative investment should consult the specific legal documentation of the relevant vehicle, where they will find the specific risks and considerations associated with that particular alternative investment. Investors should carefully review and consider potential risks before investing. No person or entity receiving this document should make an investment decision without obtaining prior and individualized legal, tax, and financial advice.

Neither AltamarCAM nor any of its group companies, nor their respective shareholders, directors, managers, employees, or advisors assume any responsibility for the integrity or accuracy of the information contained herein, nor for any decisions made by recipients of this document based on it or on the information it contains.

This document is strictly confidential and may not be reproduced or disclosed in any manner, in whole or in part, without the prior written consent of AltamarCAM.