Infrastruktur – Eine Grundsolide Asset-Klasse

Infrastruktur ist eine Asset-Klasse, die sowohl für die Gewährleistung der Wettbewerbsfähigkeit als auch die Bereitstellung grundlegender Dienstleistungen in Volkswirtschaften unerlässlich ist. Im aktuellen Umfeld überzeugt sie mit planbaren langfristigen Cashflows und dadurch mit hoher Resilienz und geringer Volatilität.

Die Erträge basieren meist auf Verträgen und Geschäftsmodellen, die an die Inflation gekoppelt sind. Infrastrukturinvestments sind normalerweise langfristig angelegt und in Ihrer Finanzierungsstruktur gegen Zinsschwankungen abgesichert. Zudem profitiert bestehende Infrastruktur in Zeiten höherer Inflation und gestörten Lieferketten von gestiegenen Baukosten für neue Infrastrukturprojekte.

Infrastruktur als Asset-Klasse umfasst Vermögenswerte, die nicht nur die Grundversorgung mit z.B. Strom, Wasser und Telekommunikationsdiensten sicherstellen, sondern auch grundlegend die Wettbewerbsfähigkeit einer Volkswirtschaft stärken. Wesentliche Grundmerkmale sind:

- Infrastruktur ist kapitalintensiv und wird in erheblichem Umfang mit Fremdkapital finanziert.

- Den meisten Infrastruktur-Assets liegen langfristige inflationsindexierte Verträge zugrunde.

- Die Bewertung von Infrastruktur-Investments erfolgt durch Abzinsung künftiger Cashflows unter Berücksichtigung der Marktzinsen.

Doch was bedeutet das im derzeitigen makroökonomischen Umfeld – mit nachlassendem Wachstum, anziehender Inflation und steigenden Zinsen?

Positive Aspekte:

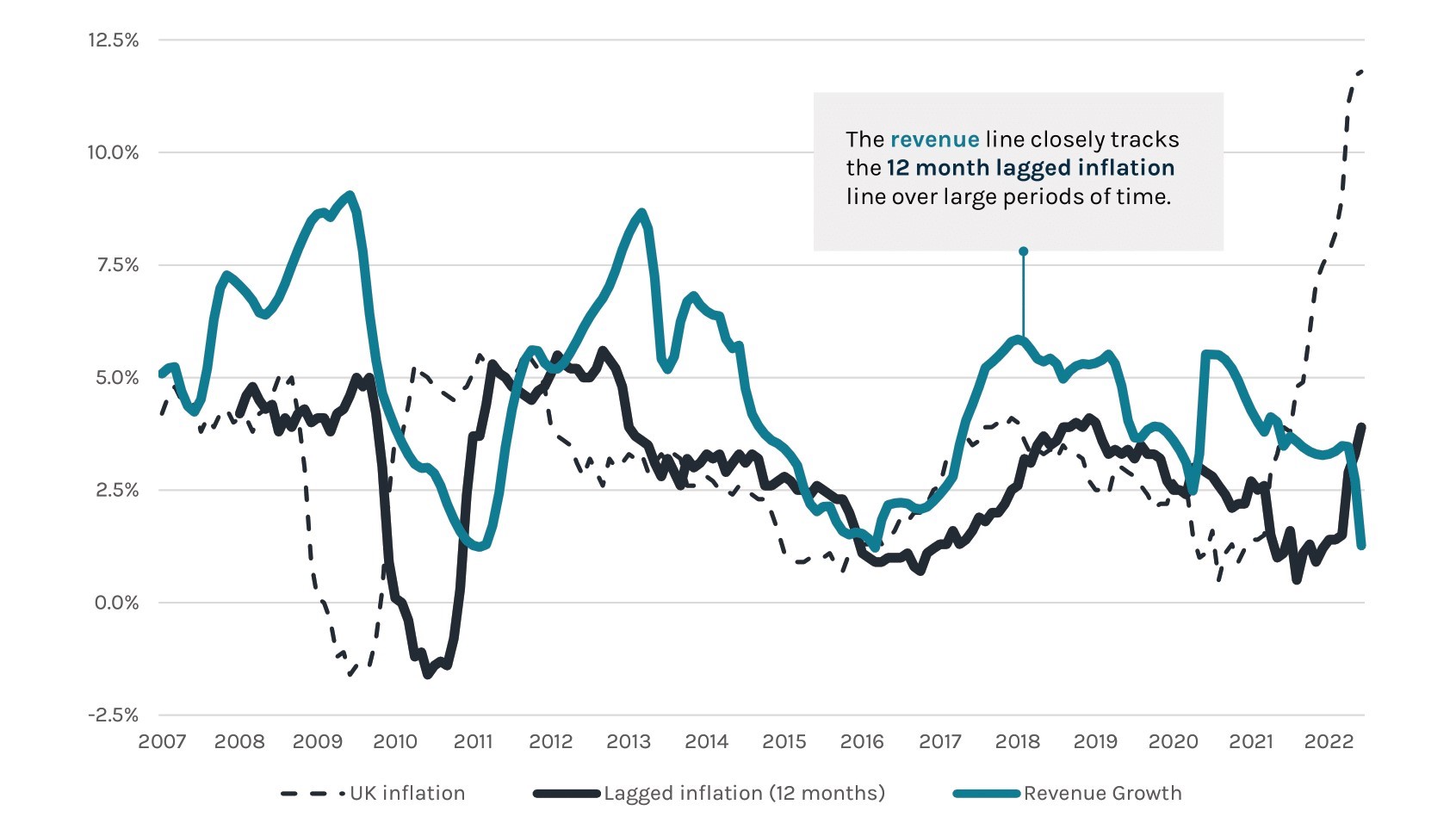

- Inflationsschutz– Die Erträge basieren meist auf Verträgen und Geschäftsmodellen, die an die Inflation gekoppelt sind; dies wird in der folgenden Grafik deutlich, die das Ertragswachstum einer Stichprobe nicht börsennotierter Infrastrukturunternehmen aus Großbritannien im Vergleich zu einer zeitversetzten Inflationskurve zeigt:

Einfluss der Inflation auf Infrastrukturerträge

Quelle: EDHEC Private UK Infrastructure Companies 2007-2021; gleitender Zwölfmonatsdurchschnitt des Umsatzwachstums und Inflationsveränderung („RPI“)

- Hoher Anteil festverzinslichen Fremdkapitals – Infrastruktur-Investments sind normalerweise langfristig angelegt. Die Fremdfinanzierung ist in der Regel so angelegt, dass der Großteil zu fest vereinbarten Zinssätzen oder gegen Zinsschwankungen abgesichert ist.

- Steigende Wiederbeschaffungskosten bestehender Assets – Durch die hohe Inflation und Störungen in den Lieferketten wird der Bau neuer Infrastruktur teuer, wodurch wiederum die Attraktivität bereits vorhandener Assets deutlich steigt.

- Höhere Zinsen lassen der öffentlichen Hand weniger finanziellen Spielraum für neue Infrastruktur – Bei steigenden Zinsen muss der Fiskus kürzertreten, sodass privaten Investoren eine umso wichtigere Rolle zukommt.

- Steigende Zinsen können die Bewertungen belasten: Auch wenn Infrastruktur-Investments über einen impliziten Inflationsschutz verfügen, können höhere Zinsen den Bewertungen schaden. Kurzfristige Zinsschwankungen werden jedoch teilweise abgefedert, weil die Abzinsungssätze auf langfristigen Durchschnittssätzen basieren.

- Bei stark fremdfinanzierten Assets mit kurzer Laufzeit sind ein Anstieg der Finanzierungskosten und ein Wertverfall nicht unwahrscheinlich. Investment-Manager versuchen daher, durch langfristige Finanzstrukturen mit unterschiedlichem Rang in der Kapitalstruktur und gestaffelten Laufzeiten das kurzfristige Refinanzierungsrisiko zu begrenzen.

- Ein Blick in die Vergangenheit zeigt, dass Infrastruktur-Assets in längeren Phasen hoher Zinsen und niedriger Inflation an Wert verlieren können. Das war beispielsweise von 1982 bis 1986 der Fall.

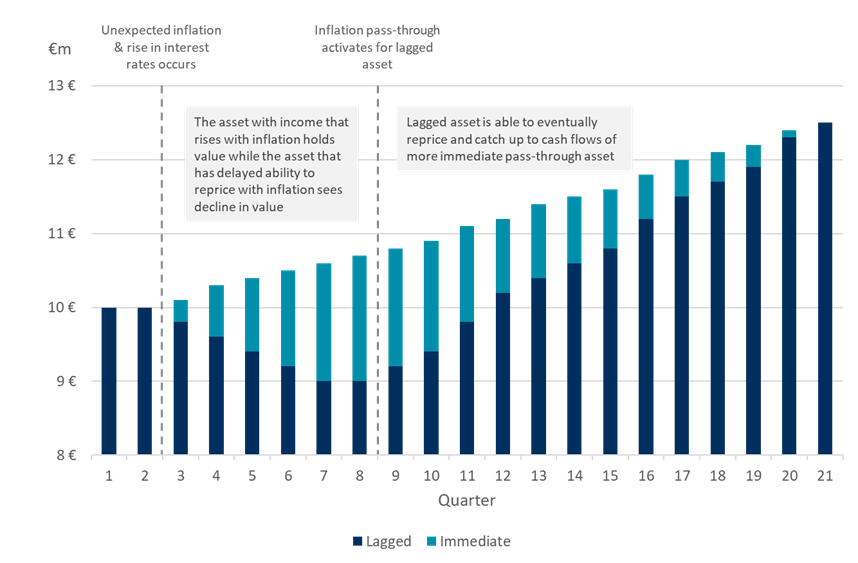

Einfluss der Inflation auf Infrastruktur-Investments: Tempo der Preisanpassungen

Quellen: Analyse von AltamarCAM, Ares Infrastructure

Bei hoher Inflation und steigenden Zinsen kommt es für die kurzfristige Werterhaltung ganz klar auf schnelle Preisanpassungen an.

Nicht börsennotierte Infrastruktur-Investments dienen also der Grundversorgung der Gesellschaft, weisen eine geringe Volatilität auf und verfügen zugleich über einen imanenten Inflationsschutz, der höhere Zinsen und Finanzierungskosten auffängt. Außerdem bieten sie die Resilienz1 und Stabilität, die es braucht, um den aktuellen makroökonomischen Herausforderungen die Stirn zu bieten.

- Aus der Wertentwicklung in der Vergangenheit lässt sich nicht zwangsläufig auf die Wertentwicklung der Zukunft schließen, denn die aktuellen wirtschaftlichen Rahmenbedingungen sind nicht mit der Wertentwicklung in der Vergangenheit vergleichbar, die sich möglicherweise nicht wiederholen wird.

WICHTIGE HINWEISE:

Dieses Dokument wurde von Altamar CAM Partners S.L. (zusammen mit seinen Tochtergesellschaften „AltamarCAM“) ausschließlich zu Informations- und Illustrationszwecken sowie als allgemeiner Marktkommentar erstellt und ist ausschließlich für die Verwendung durch den Empfänger bestimmt. Wenn Sie dieses Dokument nicht von AltamarCAM erhalten haben, sollten Sie es nicht lesen, verwenden, kopieren oder weitergeben.

Die hierin enthaltenen Informationen spiegeln die Ansichten von AltamarCAM zum Zeitpunkt dieses Dokuments wider, die sich jederzeit und ohne Vorankündigung ändern können, ohne dass eine Verpflichtung zur Aktualisierung besteht oder sichergestellt wird, dass Sie über etwaige Aktualisierungen informiert werden.

Dieses Dokument basiert auf Quellen, die als zuverlässig angesehen werden, und wurde mit größtmöglicher Sorgfalt erstellt, um zu vermeiden, dass es unklar, zweideutig oder irreführend ist. Es wird jedoch keine Zusicherung oder Garantie hinsichtlich seiner Wahrhaftigkeit, Genauigkeit oder Vollständigkeit gegeben, und Sie sollten nicht davon ausgehen, dass dies gegeben ist. AltamarCAM übernimmt keine Verantwortung für die in diesem Dokument enthaltenen Informationen.

Dieses Dokument kann Prognosen, Erwartungen, Schätzungen, Meinungen oder subjektive Einschätzungen enthalten, die auch als solche zu verstehen sind und niemals als Zusicherung oder Garantie für gegenwärtige oder zukünftige Ergebnisse, Erträge oder Gewinne. Soweit dieses Dokument Aussagen über die künftige Entwicklung enthält, sind diese Aussagen zukunftsgerichtet und unterliegen einer Reihe von Risiken und Unwägbarkeiten.

Bei diesem Dokument handelt es sich lediglich um einen allgemeinen Marktkommentar, der in keiner Weise als einer Regulierung unterliegende Beratung, Anlageangebot, Aufforderung oder Empfehlung zu verstehen ist. Alternative Anlagen können hochgradig illiquide sein, sind spekulativ und eignen sich möglicherweise nicht für alle Anleger. Investitionen in alternative Anlagen sind nur für erfahrene und versierte Anleger gedacht, die bereit sind, die mit einer solchen Anlage verbundenen hohen wirtschaftlichen Risiken zu tragen. Potenzielle Anleger einer alternativen Anlage sollten den jeweiligen Fondsprospekt und die Bestimmungen lesen, in denen die spezifischen Risiken und Überlegungen im Zusammenhang mit einer bestimmten alternativen Anlage beschrieben sind. Die Anleger sollten die potenziellen Risiken sorgfältig prüfen und abwägen, bevor sie investieren. Keine natürliche oder juristische Person, die dieses Dokument erhält, sollte eine Investitionsentscheidung treffen, ohne zuvor eine rechtliche, steuerliche und finanzielle Beratung auf einer spezifizierten Basis erhalten zu haben.

Weder AltamarCAM noch seine Konzerngesellschaften oder deren jeweilige Anteilseigner, Direktoren, Manager, Angestellte oder Berater übernehmen irgendeine Verantwortung für die Integrität und Richtigkeit der hierin enthaltenen Informationen oder für die Entscheidungen, die die Adressaten dieses Dokuments auf der Grundlage dieses Dokuments oder der hierin enthaltenen Informationen treffen könnten.

Dieses Dokument ist streng vertraulich und darf ohne die vorherige schriftliche Zustimmung von AltamarCAM weder ganz noch teilweise vervielfältigt oder in irgendeiner anderen Weise veröffentlicht werden.